Overview

The crypto market spent the week moving between relief and restraint. Bitcoin and Ethereum both rebounded from early-week stress, yet neither asset delivered a clean trend confirmation strong enough to fully shift the broader structure out of consolidation. The week began with geopolitical tension, volatile oil pricing, and a market still sensitive to the idea that rates may stay higher for longer. It ended with renewed ETF demand, calmer risk appetite, and a visible rebound across major tokens, but the move still looked more like a recovery inside a range than the start of a fully re-accelerating cycle. Bitcoin traded roughly between $70.6K and $78.3K during the week, while Ethereum moved in an approximately $2.18K to $2.46K band.

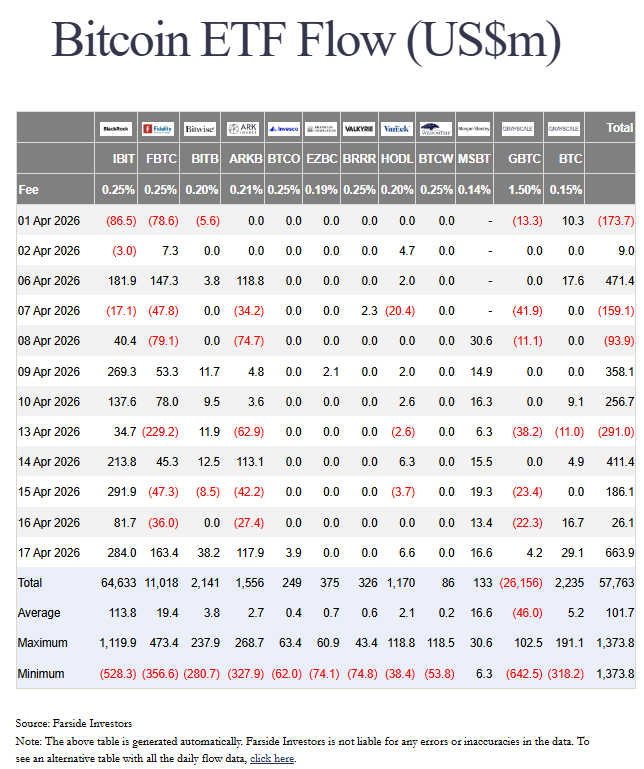

The clearest flow conclusion was that institutional demand returned through regulated channels, especially U.S. spot ETFs, but the preference remained concentrated in large, liquid assets rather than broad altcoin expansion. For the tradable U.S. ETF sessions in the same week, spot Bitcoin ETFs still finished with about $996.5 million in net inflows despite a sharp outflow on April 13, while spot Ethereum ETFs added about $275.9 million. That combination supported price recovery, but it did not yet produce a broad-based rotation across the rest of the market.

BTC

Bitcoin remained the market’s primary anchor. After opening the week under pressure near the lower end of the weekly range, it recovered quickly and briefly pushed above $78K before settling back toward the mid-$75K area by April 19. That pattern matters: the market did show buyers on weakness, but it also showed that strength above the upper-$70K area still attracts supply. In practical terms, Bitcoin spent the week reclaiming damaged ground rather than establishing a fresh directional breakout.

What kept Bitcoin relatively firm was not a sudden shift into speculative excess, but the combination of restored ETF demand and improving late-week risk sentiment. This is a constructive signal for market structure because it shows that institutional allocation did not disappear during the recent macro shock. At the same time, Bitcoin still traded like a macro-sensitive risk asset. That means the path higher remains dependent not only on crypto-native demand, but also on whether inflation pressure, oil volatility, and policy expectations become less restrictive.

ETH

Ethereum followed the same broad direction as Bitcoin, but with a slightly more conditional tone. It recovered from an early-week low near $2.18K, pushed to roughly $2.46K on April 17, and then eased back toward the low-$2.3K area by the end of the week. The rebound was real, and ETF demand clearly improved, but Ethereum still did not take leadership away from Bitcoin in a decisive way. The market treated ETH as a participating asset in the rebound, not yet as the main destination for fresh capital.

That distinction is important. Ethereum’s positive ETF flows show that institutional participation in ETH remains active, and the week’s recovery suggests that buyers are still willing to add exposure at compressed levels. Even so, the broader market narrative remains more concentrated in Bitcoin-led positioning. Until Ethereum can convert improving flows into clearer relative strength and sustained follow-through, it is more accurate to describe ETH as recovering inside the broader market move than driving it.

Institutional actions

Institutional behavior was one of the most important stabilizing forces this week. Spot Bitcoin ETFs shifted from a large single-day outflow on April 13 to strong inflows on the following sessions, culminating in a $663.9 million daily net inflow on April 17. Spot Ethereum ETFs also stayed positive across the week’s key sessions, closing April 17 with a $127.4 million daily net inflow. This matters because it shows that institutional buyers were willing to re-engage even while macro uncertainty remained unresolved.

The institutional story also broadened beyond daily flow data. On April 14, Goldman Sachs filed for its first bitcoin ETF product, adding another signal that major financial firms continue to build structured exposure around Bitcoin despite the market’s more difficult year-to-date backdrop. Taken together, the week suggested that institutional interest is still present, but it is expressing itself through regulated, familiar wrappers and mostly around Bitcoin first, Ethereum second.

Regulatory & policy

This week’s policy backdrop was active, but not in a way that produced a single immediate pricing catalyst. In the UK, the Financial Conduct Authority launched a consultation on proposed crypto rules covering trading platforms, custody, staking, and safeguarding. In Europe, France’s finance minister publicly pushed for a stronger euro-stablecoin ecosystem, highlighting the strategic competition now developing around digital payments infrastructure. These are not short-term price triggers on their own, but they do show that regulatory development is continuing and increasingly tied to financial sovereignty, market structure, and payment rails rather than only enforcement headlines.

At the same time, the broader policy environment remains incomplete. Progress on global stablecoin standards was described by the Bank of England’s Andrew Bailey as having slowed, and in the U.S., digital-asset market structure still lacks full finality even though legislative pressure for clarity remains in place. For markets, that means the long-term direction of regulation is improving in some jurisdictions, but the near-term environment still does not provide the kind of fully settled framework that would justify immediate repricing across the entire sector.

Macro linkage

Macro remained the ceiling on enthusiasm. Early in the week, the oil shock linked to Middle East developments reinforced the risk that inflation could stay sticky and policy easing could remain delayed. St. Louis Fed President Alberto Musalem said the oil shock was likely to keep core inflation near 3% and rates on hold for some time. That is exactly the kind of backdrop that tends to limit clean upside in liquidity-sensitive assets, including crypto.

Later in the week, market tone improved as hopes for de-escalation helped oil stay below $100 and pushed global equity funds into a fourth straight week of inflows. Even so, the macro picture did not become fully supportive. IMF and World Bank meetings underscored how geopolitical shocks are still constraining growth expectations and keeping energy volatility central to the global outlook. For crypto, the implication was clear: risk appetite improved enough to support a rebound, but not enough to remove the macro overhang.

Altcoins

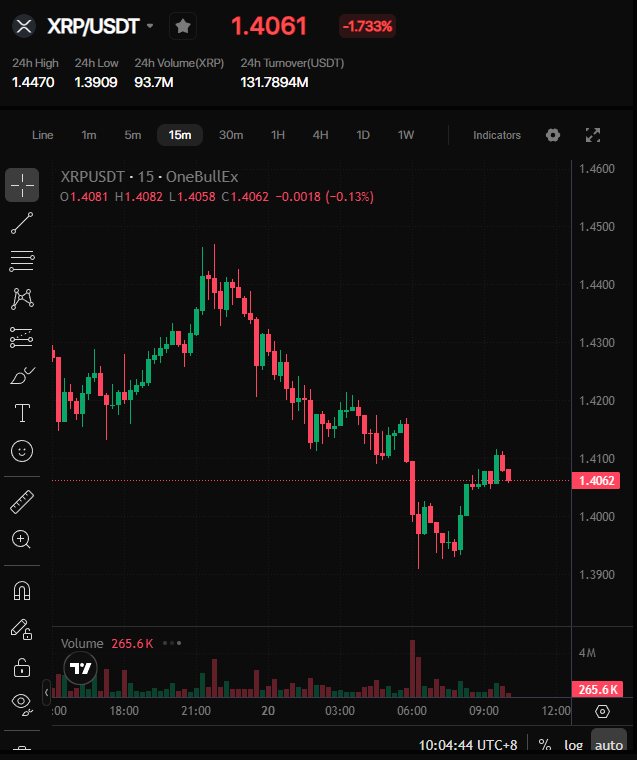

Altcoins participated in the rebound, but leadership remained narrow. XRP was one of the stronger large-cap performers during the week, with price action moving from roughly $1.32 to just above $1.50 at the weekly high, while Solana traded in an approximately $81.5 to $90.7 range. DOGE also bounced sharply into the late-week relief move, briefly trading above $0.10 before easing back. These moves show that traders were willing to add selective beta once macro fear cooled, but the market still did not rotate into a broad, durable altcoin expansion.

That distinction remains important for positioning. A narrow rebound led by majors and a few liquid altcoins is not the same as a broad alt-season. Volume and conviction were still selective, and the week’s better altcoin performance looked more like tactical participation in a Bitcoin-led recovery than a new market phase with independent leadership across the board.

OneBullEx view

From OneBullEx’s perspective, the market ended the week in better shape than it began, but the bigger message is still one of consolidation rather than clean expansion. ETF flows improved materially, Bitcoin reasserted itself as the primary institutional destination, and Ethereum participated with healthier demand than the market had shown earlier in the month. Even so, macro sensitivity remains high, and the combination of oil-driven inflation risk, uncertain policy timing, and uneven altcoin participation argues against reading this week as a full risk-on reset. The more disciplined interpretation is that the medium-term structure remains intact, but upside still needs confirmation through sustained follow-through rather than headline-driven spikes. In that environment, selective positioning, strong liquidity preference, and measured risk management remain the more credible approach than aggressive chasing at the top of short-term rebounds.

Comments

0 comments

Please sign in to leave a comment.